TL;DR:

- Luxury assets on the French Riviera serve as vital instruments for wealth preservation, income generation, and intergenerational legacy. Their value is driven by scarcity, provenance, and lifestyle integration, making them resilient across economic cycles. Successful ownership requires intentional management, expert structuring, and disciplined stewardship to maximize long-term benefits.

There is a persistent misconception that luxury assets exist purely as a theatre of wealth, gleaming trophies displayed for admiration rather than purpose. The truth, as generations of astute families along the Côte d’Azur have quietly demonstrated, is far more compelling. A cliff-top villa above Èze, bathed in the golden light that inspired Nietzsche himself, is not simply a residence. It is a living instrument of wealth preservation, an heirloom calibrated to outpace inflation, generate meaningful income, and pass seamlessly to the next generation. This guide reveals the strategic power of luxury assets and how to hold them with the intentionality they deserve.

Table of Contents

- What defines a luxury asset: more than meets the eye

- Core advantages: legacy, resilience, and income

- Scarcity, provenance, and value retention

- Risks, limitations, and the art of holding

- Practical strategies: making luxury assets work for you

- Why intentional, expert-driven ownership beats luck every time

- Looking to secure your legacy on the Côte d’Azur?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Luxury assets provide resilience | They protect family wealth from inflation and market shocks through tangible, scarce value. |

| Legacy planning is vital | Careful structuring and expert advice secure luxury assets for future generations. |

| Illiquidity is a double-edged sword | While it can protect against panic selling, forced sales or poor planning expose owners to risk. |

| Ongoing management wins | Exceptional results come from expert, intentional holding and not from luck or neglect. |

What defines a luxury asset: more than meets the eye

To ground our discussion, we must first define what counts as a luxury asset and why it matters for your long-term goals. The term encompasses a broad and varied universe, ranging from prime coastal real estate in Antibes or Cap d’Antibes, to museum-quality art, rare vintage watches, classic automobiles, and fine wines. What unites them is not price alone. It is the combination of scarcity, provenance, and genuine desirability that endures across economic cycles.

For high-net-worth families, real estate on the French Riviera occupies a singular position within this universe. A property overlooking Cannes’ Croisette or nestled within the lemon-scented lanes of Menton offers something no equity portfolio can: tangible presence, personal use, and rental income. As research confirms, luxury real estate functions as a tangible, experience-bearing asset that also diversifies away from traditional stocks and bonds, reducing overall portfolio volatility in ways that paper assets simply cannot replicate.

Common myths deserve to be addressed directly. Many people assume that luxury assets are illiquid luxuries reserved for those who can afford to park capital indefinitely. In reality, a thoughtfully chosen villa on Mont Boron in Nice, or a newly completed sea-view apartment in Sainte-Maxime, can generate 3–5% in elite holiday lets whilst simultaneously appreciating in underlying value. Understanding the personalised luxury benefits of your chosen asset class is the first step towards building a genuinely resilient portfolio.

Key qualities that distinguish a true luxury asset from a mere expensive purchase include:

- Scarcity: Limited supply in desirable locations such as Monaco-adjacent plots or Cap d’Antibes coastal sentiers

- Provenance: A documented history of ownership, craftsmanship, or architectural significance

- Income potential: Capacity to generate returns through seasonal or long-term letting

- Lifestyle integration: The ability to serve as a personal sanctuary whilst functioning as an investment

Staying across evolving luxury buyer trends is equally essential, as shifting demand patterns directly influence which assets hold their value most reliably.

“The finest luxury assets are not purchased. They are curated with intention, held with patience, and ultimately passed down as the most eloquent expression of a family’s values.”

Core advantages: legacy, resilience, and income

Now that we understand what luxury assets are, let’s explore their substantial advantages for discerning investors. The Riviera’s finest properties have a compelling track record: villas in established enclaves typically appreciate at 5–8% annually, and that growth compounds powerfully over generational holding periods.

Luxury real estate preservation is widely positioned as an inflation hedge and a long-term wealth-preservation tool for legacy planning, particularly as central banks ease rates in 2026 and capital seeks tangible stores of value. When inflation erodes the purchasing power of cash and bonds, a stone-built Provençal mas in the hills above Antibes tends to hold its worth with quiet authority.

The following table compares three core luxury asset classes across the dimensions most relevant to legacy-focused investors.

| Asset class | Diversification | Income potential | Tangibility | Legacy transfer |

|---|---|---|---|---|

| Prime real estate | High | High (3–5% rental yield) | Physical and experiential | Excellent via succession structures |

| Fine art | Moderate | Low (unless loaned) | Physical and cultural | Good, though valuation complex |

| Rare collectibles | Moderate | Very low | Physical only | Moderate, estate planning essential |

What the table makes clear is that Riviera real estate leads across every dimension that matters most to families focused on wealth protection and intergenerational transfer. Holiday rentals boost returns substantially when managed professionally, transforming what might otherwise be a dormant asset into an income-generating machine that also funds its own maintenance and holding costs.

There is also an experiential dimension that no financial instrument can offer. Imagine greeting the summer season from a terrace above Sainte-Maxime, watching ferries glide towards Saint-Tropez as the evening light turns the Gulf of Saint-Tropez to hammered gold. That lived experience becomes part of the asset’s story, woven into the legacy and ROI that families discuss across generations.

Pro Tip: Engage a specialist estate planning attorney in the early stages of any luxury property acquisition. Structures such as Sociétés Civiles Immobilières (SCIs) in France can dramatically simplify succession, reduce inheritance tax exposure, and protect the asset from forced sale scenarios that could otherwise erode decades of accumulated value.

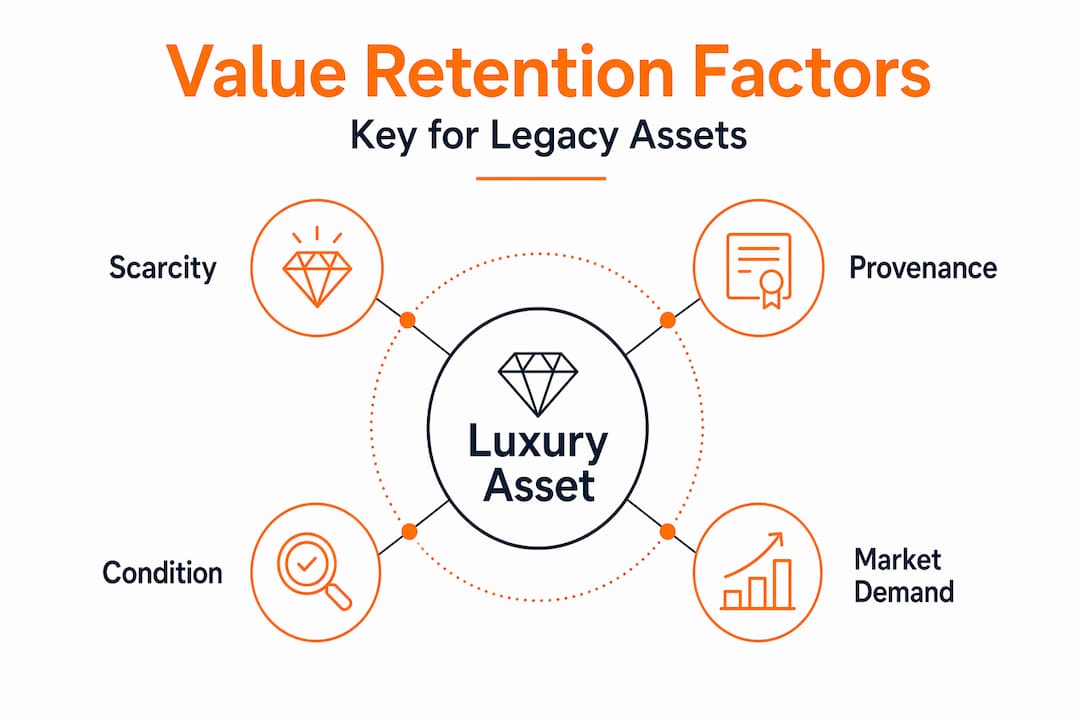

Scarcity, provenance, and value retention

Beyond the basic advantages, what makes certain luxury assets truly exceptional at retaining value? The answer lies in two intertwined forces: scarcity and provenance. These are the twin engines that have driven Riviera property values through the oil crises of the 1970s, the global financial crisis of 2008, and the pandemic disruptions of 2020 and beyond.

Research from Forbes confirms that luxury asset value retention across both real estate and collectible markets depends critically on scarcity and provenance, and on the ability to manage sale friction and illiquidity with discipline. In other words, rare locations hold value; common ones do not.

On the Côte d’Azur, specific indicators of superior value retention include:

- Irreplaceable location: Beachfront positions in Cannes, sea-view plots in Nice’s Château Hill quarter, or private Cap d’Antibes estates where no new supply is physically possible

- Architectural heritage: Belle Époque villas with original period features, or Picasso-era buildings in Antibes’ old town with documented cultural significance

- Eco-credentials: Properties with solar arrays, green certifications, and biophilic design elements, which command a premium as sustainability-conscious heirs inherit wealth

- Privacy and exclusivity: Gated estates, private beach access, or off-market properties known only within elite circles

Our value curation guide explores in detail how each of these criteria translates into measurable price resilience over time. For buyers considering off-plan projects such as the new designer apartments near Sainte-Maxime’s Nartelle beach, provenance is being built in real time through architectural distinction and the cachet of a premier Riviera address.

Fine art and rare watches behave similarly. A Basquiat acquired in 2006 and held through 2026 would have vastly outperformed a mid-tier bond portfolio. The principle is identical to holding a Belle Époque villa in Menton through the same period: scarcity, cultural significance, and sustained global demand create a floor beneath the price that broad market selloffs simply cannot reach.

Risks, limitations, and the art of holding

Understanding advantages must also include how to sidestep potential pitfalls in holding luxury assets. Even the most carefully chosen Riviera villa carries risks that, if ignored, can quietly transform an heirloom into a liability.

The primary risks, in order of severity, are:

- Illiquidity: Luxury real estate cannot be sold in an afternoon. In a disrupted market, finding the right qualified buyer may take months or longer.

- Forced sale timing: A family liquidity crisis, divorce settlement, or poorly structured estate can compel a sale at precisely the wrong moment in the market cycle.

- Holding costs: Property taxes, maintenance, insurance, management fees, and renovation programmes accumulate relentlessly. Left unmanaged, they consume net returns.

- Market cycle misreading: Even prime Riviera property moves in cycles. Buying at peak sentiment in a micro-location without broader demand can result in years of stagnation.

- Behavioural risk: Emotional attachment to an asset can prevent owners from making rational decisions about refinancing, letting, or eventual sale.

As Fiducient Advisors make clear, wealth protection benefits can be seriously undermined by illiquidity and behavioural or timing risk, especially when a family’s liquidity needs or tax and financing constraints force a sale during periods of stress.

“The wealthiest families we work with do not simply own magnificent properties. They maintain them with structured discipline, hold adequate liquidity buffers, and plan their exits with the same care they applied to their acquisitions.”

Understanding liquidity challenges in private real estate markets helps investors calibrate their expectations and plan their broader financial architecture accordingly. A Côte d’Azur estate should form one layer of a diversified wealth structure, not the entirety of it.

Pro Tip: Before completing any luxury property acquisition, stress-test your liquidity position. Ensure you hold sufficient accessible reserves to cover three to five years of holding costs without needing to touch the asset. This single discipline eliminates the most common source of forced, value-destroying sales.

Review your investment risk factors carefully, and consider the duration of luxury market cycles before committing capital. Professional property management for legacy assets is not an optional extra. It is a foundational part of the holding strategy.

Practical strategies: making luxury assets work for you

So, how do you ensure luxury assets deliver their full long-term advantage? Here’s how to put best practices to work for your legacy, drawing on the approaches used by the most successful families we work with on the Riviera.

As confirmed by leading advisers, full-cycle ownership costs for luxury assets must incorporate estate-structure considerations and constraints on exit timing, particularly for non-financial assets such as art, watches, and prime real estate. Ignoring these factors at acquisition leads to unpleasant surprises at disposition.

A structured approach to optimising luxury asset holdings involves the following core disciplines:

- Engage local and international specialists: French notaires, tax advisers familiar with cross-border estate law, and experienced Riviera property managers form the essential team for any serious investor

- Review holding periods honestly: Define at acquisition whether the asset is a 10-year, generational, or indefinite hold, and structure financing and tax arrangements accordingly

- Map liquidity needs against asset illiquidity: Ensure liquid assets elsewhere cover all foreseeable capital requirements, so the luxury property never becomes a forced sale scenario

- Assess estate and tax implications early: Inheritance tax rules vary significantly between France, the UK, and other jurisdictions; early structuring can preserve hundreds of thousands in value

- Set clear legacy aims: Decide whether the asset is intended as a family holiday home, a rental yield generator, a capital appreciation play, or all three simultaneously, and manage it accordingly

Learning how to evaluate luxury investments with rigour is a skill that distinguishes successful legacy builders from those who simply own expensive properties. For those navigating the process from overseas, our guidance on international luxury property buying in 2026 covers the key legal, financial, and procedural steps in detail.

Regularly re-evaluating property values with certified independent appraisers is equally important. The Riviera market is dynamic: Antibes’ yacht-dotted marina quarter has appreciated differently from the hillside villages above Menton, and what held true three years ago may no longer reflect current demand patterns.

Why intentional, expert-driven ownership beats luck every time

We have worked with enough families along the Côte d’Azur to observe a pattern that mainstream financial media rarely discusses. The real dividing line in luxury asset performance is not which property you buy. It is whether you own it intentionally or accidentally.

Accidental ownership is more common than you might expect. A family inherits a Provençal mas near Antibes, lacks a clear plan for managing it, allows holding costs to accumulate, and eventually sells under pressure at a price far below what structured, informed management would have produced. The asset was magnificent. The stewardship was not.

Contrast this with the families who acquire a sea-view villa near Menton with a clear SCI structure in place, a professional property manager generating seasonal rental income throughout the Cannes Film Festival season and the Saint-Tropez summer, a liquidity reserve held separately, and a succession plan already registered with their notaire. These families compound quietly and powerfully, decade after decade.

As research makes plain, ‘paper’ value can diverge profoundly from true outcome if holding costs, taxes, illiquidity, and succession plans are not being actively managed. The theoretical valuation on a notaire’s balance sheet and the actual net wealth delivered to the next generation can differ by millions, depending entirely on the quality of stewardship in between.

Our philosophy at Living on the Côte d’Azur is built around this conviction. Curating high-value real estate is not simply about sourcing exceptional properties, though we do that exceptionally well. It is about accompanying clients through the entire ownership journey, from initial acquisition strategy to succession planning, so that the asset delivers its full promise across generations. Luck favours the prepared. Lasting legacy favours the intentional.

Looking to secure your legacy on the Côte d’Azur?

If you are serious about leveraging luxury assets for legacy, expert guidance on the Côte d’Azur is key to turning insight into lasting impact. At Living on the Côte d’Azur, we bring together an intimate knowledge of the Riviera’s finest locations, from Menton’s lemon-festival streets to the private coves of Cap d’Antibes, with a deeply personalised approach to legacy-focused wealth protection. Our curated portfolio spans luxury villas for sale across the French Riviera, including off-market properties unavailable to the general market. We also accept cryptocurrency payments, making us the natural partner for digital-era wealth holders. Explore your investment options on the Côte d’Azur and begin building the legacy your family deserves.

Frequently asked questions

How do luxury assets protect against inflation?

Luxury real estate and select collectibles often retain value during inflationary periods due to their scarcity and lasting demand, making them a reliable store of wealth when currency purchasing power weakens.

Are luxury assets truly liquid when you need to sell?

Luxury assets are famously less liquid than stocks or bonds; as research confirms, collectibles and prime real estate carry high entry and exit costs, meaning selling quickly during market disruptions is both difficult and potentially value-destructive.

What is the main risk of holding luxury property versus traditional investments?

The largest risk is illiquidity: as advisers warn, wealth protection benefits can be undermined by timing and behavioural risk when liquidity constraints force a sale at the wrong moment in the market cycle.

How do holding costs affect luxury assets?

Holding costs including management fees, property tax, insurance, and maintenance can significantly erode net returns if not planned for at acquisition, as full-cycle ownership costs must be factored into any honest assessment of long-term profitability.

Recommended

//

//