TL;DR:

- Proper legal and tax structuring, such as using SCIs, is essential for building wealth and legacy on the Côte d’Azur.

- Understanding French inheritance laws and tax exemptions helps protect assets across generations.

- Diversifying properties by location, type, and rental strategy enhances portfolio resilience and rental income.

Acquiring a magnificent villa above the Côte d’Azur coastline, where the salt-kissed air mingles with the scent of Provençal lavender, is a profound moment. Yet the uncomfortable truth is that many high-net-worth investors mistake the act of purchase for the act of strategy. On the French Riviera, where prestige properties consistently appreciate 5–8% annually and seasonal rental demand peaks during Cannes Film Festival, Monaco Grand Prix weekends, and Saint-Tropez’s golden summer months, the real wealth is built not in the acquisition itself, but in how that acquisition is legally framed, tax-optimised, and woven into a generational legacy plan from the very first signature.

Table of Contents

- Understanding key tax structures for luxury portfolios

- Legal frameworks and ownership structures

- Portfolio diversification and seasonal rental strategy

- Safeguarding and optimising your legacy

- Our perspective: true legacy requires structure, foresight, and local expertise

- Connect with Côte d’Azur luxury portfolio advisors

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand IFI tax | The IFI applies to worldwide real estate assets over €1.3M and requires careful structuring for new residents. |

| Choose the right legal entity | Using an SCI or other legal structure helps optimise inheritance and unlocks greater flexibility. |

| Diversify for income | Strategically diversify portfolio properties and rental profiles to maximise seasonal yields and legacy value. |

| Plan for future generations | Legacy planning and compliance ensure your portfolio benefits your family and protects against legal pitfalls. |

Understanding key tax structures for luxury portfolios

Having set the stage for strategic property portfolio structuring, we now turn to the tax landscape you must navigate with precision and foresight. France’s fiscal framework for high-value real estate is sophisticated, and underestimating it can quietly erode the returns that drew you to the Riviera in the first place.

The Impôt sur la Fortune Immobilière (IFI) is the cornerstone tax that every serious investor must understand. It applies to worldwide real estate net assets exceeding €1.3M and is levied annually on French tax residents. Rates progress from 0.5% to 1.5%, meaning a portfolio valued at €5M could trigger a recurring annual liability of approximately €50,000 before any deductions. That figure alone should sharpen your focus on structuring.

There is, however, a notable exemption that works powerfully in favour of newly arriving residents. As confirmed by Expats in France, the IFI applies to worldwide real estate above €1.3M, but new French tax residents are exempt from including foreign properties for their first five years of residency. This window is a rare and valuable opportunity to reposition global holdings before full IFI exposure takes effect.

Key IFI thresholds at a glance

| Net asset value | IFI rate |

|---|---|

| Up to €800,000 | 0% |

| €800,001 to €1,300,000 | 0.5% |

| €1,300,001 to €2,570,000 | 0.7% |

| €2,570,001 to €5,000,000 | 1% |

| €5,000,001 to €10,000,000 | 1.25% |

| Above €10,000,000 | 1.5% |

The Société Civile Immobilière (SCI) is the structuring vehicle of choice for most discerning investors. It is a French civil property company that holds real estate, enabling multiple shareholders to own property collectively without the rigidity of direct ownership. Our detailed luxury real estate tax guide explores the full mechanics, but in essence, an SCI separates the individual from the asset, creating fiscal buffers and inheritance pathways that direct ownership simply cannot replicate.

Key advantages of an SCI structure include:

- Inheritance simplification: Shares in an SCI can be gifted incrementally to heirs, taking advantage of French gift tax allowances every fifteen years.

- IFI optimisation: Loans held within the SCI reduce the taxable net asset value, lowering annual liability.

- Rental income flexibility: The SCI can elect for corporation tax or income tax treatment, depending on which is more favourable for your overall fiscal position.

- Reduced notary friction: Transferring shares is less costly than transferring property directly, protecting more wealth at each generational handover.

Understanding how these structures interact with seasonal rental returns is equally important. Our property tax guide clarifies how rental income generated through an SCI is taxed differently from income earned personally, and our real estate tax investor guide provides updated 2026 guidance for those entering the market now.

Statistic callout: Properties structured correctly through an SCI can reduce effective inheritance costs by up to 40% compared to direct ownership, making the legal setup cost a highly efficient investment in itself.

Legal frameworks and ownership structures

Understanding tax is only one pillar. Legal ownership choices shape both your legacy protection and your portfolio’s long-term flexibility, and on the Côte d’Azur, where property values regularly exceed €3M for sea-view estates, every structural decision carries significant consequence.

Direct ownership, the most common approach among first-time French property buyers, is straightforward but carries limitations. Your estate enters the French succession system in full, subject to forced heirship rules that reserve portions of inheritance for biological children regardless of your wishes. For investors with blended families, international heirs, or complex cross-border portfolios, this can create disputes that take years and considerable legal fees to resolve.

The SCI, as confirmed by Expats in France, offers a cleaner structure for optimisation. Shares are distributed among family members over time, each transfer potentially falling below the threshold for inheritance tax. It is elegant, efficient, and entirely legal when managed with proper governance.

Ownership structure comparison

| Structure | Inheritance control | Tax optimisation | Rental flexibility | Setup cost |

|---|---|---|---|---|

| Direct ownership | Low | Limited | Simple | Minimal |

| SCI (income tax) | High | Moderate | Good | Moderate |

| SCI (corporation tax) | High | Strong for yield | Excellent | Moderate |

| Offshore holding company | Very high | Complex | Moderate | High |

For those with portfolios spanning multiple countries, including those investing simultaneously in Ibiza, Bali, or Mauritius alongside the Riviera, cross-border structuring becomes essential. Understanding how to finance luxury real estate in tandem with your structure can protect capital flows across jurisdictions.

The numbered steps for establishing a sound ownership framework are as follows:

- Engage a notaire and a tax attorney before signing any preliminary agreement. French property law operates through notaires, but their role is neutral; they do not advocate for your interests specifically.

- Determine your residency intentions clearly. Will you become a French tax resident? For how long? This directly dictates which IFI exemptions apply.

- Select your SCI tax regime based on rental income projections and anticipated holding period.

- Document all shareholder agreements within the SCI statutes, covering succession, decision-making rights, and exit mechanisms.

- Review forced heirship implications for your specific family situation, particularly given France’s acceptance of the EU Succession Regulation, which can allow non-French citizens to elect the law of their nationality to govern inheritance.

We strongly recommend consulting resources on forced heirship regulations before finalising any ownership structure, and our dedicated guide on real estate inheritance provides essential reading for families with complex succession needs.

Pro Tip: Register your SCI before purchasing your first Riviera property. Retroactively transferring a directly owned property into an SCI triggers additional taxes and fees that can amount to several percentage points of the property’s value.

Portfolio diversification and seasonal rental strategy

Once your legal structure is firmly in place, strategic diversification becomes the engine that drives both income and resilience. The Côte d’Azur is not a monolithic market; it is a constellation of distinct micro-markets, each with its own seasonal rhythm, buyer profile, and rental premium.

Consider how the geography itself dictates opportunity. Cap d’Antibes, where the scent of pine and sea salt mingles above hidden coves, commands some of the highest privacy premiums on the Riviera. A secluded villa here appeals to ultra-high-net-worth renters seeking discretion during the Cannes Film Festival or the Monaco Grand Prix, often letting at €50,000 or more per week during peak season. Meanwhile, Sainte-Maxime’s sun-bleached Nartelle beach draws a younger family market, with properties from €1.2M generating strong seasonal returns during the long summer months, particularly for those who want the buzz of a ferry ride to Saint-Tropez without the Tropezien price tag.

As noted by Expats in France, the IFI applies to worldwide real estate above €1.3M, exempting foreign properties for new residents during the first five years, which means thoughtful diversification across international markets during this window can reduce overall IFI exposure while building yield across multiple jurisdictions.

“The most enduring portfolios we have curated on the Riviera blend at least one legacy anchor property, held for appreciation and family use, with one or two yield-focused assets positioned for elite seasonal lets.”

Key diversification considerations for a robust Riviera portfolio:

- Blend legacy and yield assets: A grand Provençal mas near Menton, immersed in the lemon-scented calm of Val Rahmeh’s botanical gardens, functions as a family sanctuary. A sleek designer apartment in Nice’s Mont Boron neighbourhood, with panoramic Baie des Anges views, generates consistent short-term rental income.

- Vary property types: Mix standalone villas, off-plan new constructions with ten-year warranties, and smaller apartments across locations such as Cannes and Antibes to reduce market concentration risk.

- Align rental profiles with demand peaks: The Riviera’s calendar of festivals, regattas, and cultural events, from the Menton Lemon Festival in February to the Cannes Film Festival in May and the summer sailing regattas off Antibes, creates predictable peaks for premium lettings.

- Consider proximity to Monaco: Properties within easy reach of Monaco consistently command higher annual appreciation rates, often at the upper end of the 5–8% range.

Explore the full range of investment options on the Côte d’Azur on our portal, and consult our international investment guide if you are balancing Riviera assets with holdings in Dubai or Portugal.

Pro Tip: For seasonal lets generating over €23,000 per year, consider registering as a non-professional furnished rental operator (LMNP) to access beneficial tax depreciation allowances. Our financing tips for the French Riviera cover how leverage can amplify net returns under this regime.

Safeguarding and optimising your legacy

Effective diversification sets the stage for sustainable legacy. But securing it for generations requires continuous attention, disciplined reporting, and proactive optimisation at every stage of the portfolio’s life.

French inheritance law, with its deeply ingrained forced heirship provisions, is the first frontier to address. Under these rules, children hold an absolute right to a reserved portion of an estate, regardless of a will’s instructions. For a client with three children, each child is entitled to one quarter of the estate by law. Structuring through an SCI, or electing the law of your nationality under the EU Succession Regulation, gives you meaningfully greater control over how and when wealth transfers.

A clear, sequenced approach to legacy safeguarding includes the following steps:

- Draft a French-law-compliant will alongside your home country will, ensuring both are coordinated rather than contradictory.

- Use lifetime gifting within the SCI to transfer shares incrementally, taking full advantage of France’s €100,000 per parent per child gift tax allowance, renewable every fifteen years.

- Conduct annual portfolio valuations to maintain accurate IFI declarations and identify opportunities to restructure loans within the SCI, reducing net taxable assets.

- Review rental performance against benchmarks at least twice yearly, comparing occupancy rates, average weekly rates, and net yields against Riviera market data.

- Engage a specialist family office or wealth manager familiar with both French and international succession law, particularly if your heirs reside across different jurisdictions.

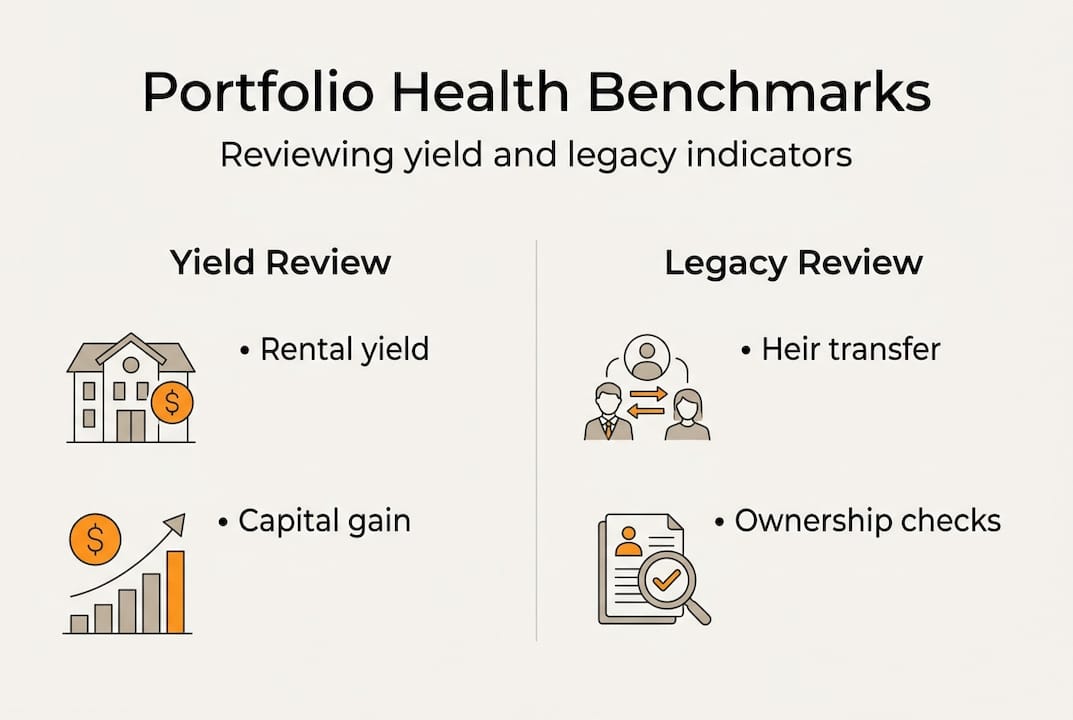

Legacy portfolio health indicators

| Indicator | Target benchmark | Review frequency |

|---|---|---|

| Annual capital appreciation | 5–8% | Annually |

| Seasonal rental yield | 3–5% net | Bi-annually |

| IFI liability as % of portfolio | Below 1% | Annually |

| Gift allowances utilised | Maximum available | Every 15 years |

| SCI share transfers completed | On schedule | As planned |

Explore our specialist resources on inheritance strategies for the Côte d’Azur and our guide to curating high-value real estate for families seeking to preserve prestige assets across generations. For a complete picture of how legacy and yield interact within a sophisticated portfolio, our legacy luxury ROI resource offers unrivalled depth.

Pro Tip: Never treat your portfolio as static. Review your SCI’s shareholder register, outstanding loans, and rental strategy every two years to capture new tax efficiencies and align with evolving French fiscal regulations, particularly as 2026 brings renewed legislative attention to high-value property taxation.

Our perspective: true legacy requires structure, foresight, and local expertise

We have observed, across many years and many pristine Riviera terraces, that the investors who build truly enduring portfolios share one quality: they resist the seduction of the acquisition alone. The view from a Cap d’Antibes clifftop villa is intoxicating. The numbers on an off-plan Mont Boron apartment are compelling. But neither the view nor the numbers protect your children’s future without the right legal architecture supporting them.

What we find most often overlooked is not the tax rate or the notaire’s fee. It is the cumulative cost of generic advice. A lawyer unfamiliar with French forced heirship nuances, or a financial adviser who does not understand SCI governance, can cost a family millions over a single generation. The Riviera is not a market for generalist strategies.

Our view is firm: the structure you choose on day one will determine whether your portfolio is a gift to your heirs or a burden. Local expertise, genuine legal nuance, and a long-term vision for legacy luxury ROI are not optional additions to your investment strategy. They are the investment strategy.

Connect with Côte d’Azur luxury portfolio advisors

Insights are powerful, but personalised support can make all the difference when structuring a portfolio designed to last generations. At Living on the Côte d’Azur, we connect discerning investors with advisors who specialise in exactly this: the convergence of legacy planning, elite seasonal rental strategy, and optimal legal structuring. Discover the world of invisible luxury real estate through our off-market portfolio, or explore the fundamentals of what constitutes a truly robust holding in our guide to luxury portfolio essentials. When you are ready to take the next step, we invite you to speak with our Côte d’Azur advisors who live and breathe this market every day.

Frequently asked questions

What is the IFI tax and who must pay it?

The IFI is the French real estate wealth tax, applied to worldwide net assets exceeding €1.3M for French tax residents. However, as confirmed by Expats in France, new residents benefit from a five-year exemption on foreign-held properties, making the timing of residency a critical planning element.

How does setting up an SCI benefit luxury property investors?

An SCI simplifies inheritance by allowing shares to be transferred incrementally to heirs, while also helping to optimise tax outcomes through loan deductions that reduce net IFI-taxable assets, making it one of the most efficient vehicles for Côte d’Azur portfolio holders.

What factors should I consider for seasonal rental income?

Prime location relative to the Riviera’s key events calendar, such as the Monaco Grand Prix, the Cannes Film Festival, and summer regattas, combined with the right property type and a professional letting management arrangement, are the most powerful drivers of consistent seasonal yield.

How do inheritance laws affect my portfolio on the Côte d’Azur?

French forced heirship rules reserve a statutory portion of your estate for biological children, which can complicate succession for families with complex structures. Properly structuring holdings through an SCI or electing an alternative national succession law under EU regulations significantly mitigates these risks and preserves your wishes for future generations.

Recommended

//

//